A Glimpse into the European Semiconductor and Emerging Technology Industries

By Dan Tracy, senior director; Christian Gregor Dieseldorff, senior analyst; Edwin Hall, senior business development manager

SEMI Industry Research & Statistics, September 20, 2007

Europe is home to more than 278 production and R&D fabs that manufacture a diverse range of integrated circuits (ICs), MEMS, power devices, compound semiconductors and innovative packages. It accounts for an estimated 12 percent of global IC fab capacity and about 30 percent of the world production for power devices. Europe is home to three world-class semiconductor R&D centers of semiconductor excellence: Inter-university Micro Electronics Center (IMEC) in Belgium, Laboratory of Electronics and Information Technology (LETI) in France, and Fraunhofer Institute in Germany. With changing markets and emerging opportunities, several device companies and a number of equipment companies have increased their involvement in the area of Microelectromechanical Systems (MEMS) and Photovoltaics (PV) manufacturing.

Source: SEMI European Microelectronics Market Study, January 2007

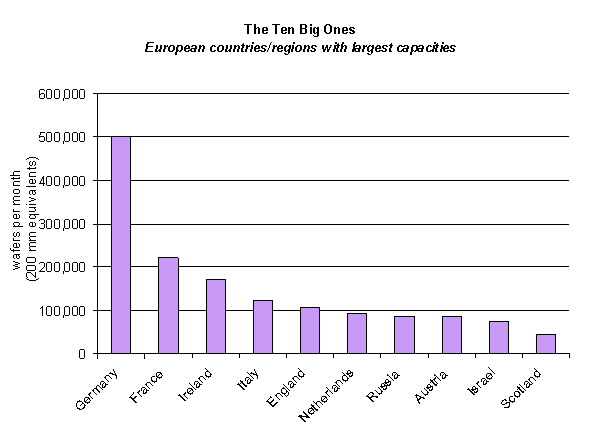

Notes: The chart includes high and low volume production fabs. A fab may be involved in several fields (technologies).

Included in this population are several 300 mm wafer fabs and several fabs with sub-90 nm technology. This diverse mix of production resources represents about $6.6 billion in semiconductor equipment and materials spending this year, making Europe a larger market than China.

For the “traditional” semiconductor IC fabs, construction spending in Europe is anticipated to reach over $700 million this year, up from last year which had over $450 million. In terms of fabs equipping, companies are expected to spend about $2.5 billion on fabs equipping, which is down compared to last year (over $3 billion). However, we expect spending to increase in 2008 by about 9 percent*.

As outlined in the Q2 ‘07 edition of the Fab Capacity database, the largest spenders in terms of fab construction projects and fabs equipping in 2007 are AMD and Intel. Numonyx, the Flash joint venture between Intel and ST Microelectronics formed in December 2006, is also expected to spend over $600M for upgrades in their Fab 18 in Kiryat Gat, Israel. We also expect the 300 mm fab (M6) in Catania, Italy, which has been an empty shell for many years and will be reactivated soon under the Numonyx joint venture. AMD is pushing out the completion of the 300mm conversion from Fab 30 to Fab 38 in Dresden into 2008.

In 2007 the four companies responsible for most of the fab capacity in Europe are, as expected, Infineon, Intel, NXP and STMicroelectronics. Together they have a capacity of over 700,000 wafers per month (in 200 mm equivalents) accounting for over 41 percent of all European fab capacity. It will be interesting to see how these and other fabs play out in the coming months.

Comparing the fab capacities within Europe, Germany, France, and Ireland are countries with the largest capacities. Dresden in Germany is considered to be the hot spot with Infineon, Qimonda and AMD leading fab companies. Ireland is lead by Intel who maintains two 12-inch fabs and one 8-inch fab in Lexlip, Ireland. In France, ST Microelectronics, Altis, Atmel and Freescale are the leading fabs providing most of capacity. ST Microelectronics is also leading in Italy followed by Micron and Numonyx.

Source: SEMI Fab Capacity Report, July 2007 Edition

As for the PV market, it is estimated that the global solar photovoltaic market in excess of $7 billion, will grow to over $16 billion in 2012. SEMI has identified close to 200 companies globally that produce manufacturing equipment for the PV market and almost 100 of those companies are headquartered in Europe, with many semiconductor suppliers diversifying into photovoltaics. These companies are using their semiconductor experience to build state-of-the-art production systems and facilities to efficiently produce PV cells and modules.

The MEMS equipment market reached $646 million worldwide in 2006:

- $338 million is equipment used in front-end processing (52%)

- $203 million for assembly, packaging and test back-end processing (32%), and

- $105 million (approximately) are R&D tools (16%).

The MEMS equipment market is expected to expand to $838 million in 2009 and $999 million in 2011. The five-year CAGR forecast for MEMS equipment is 9%. According to the January European Microelectronics Market Study, Europe accounts for 16% of MEMS worldwide sales and Germany has the highest number of MEMS fabs. STMicroelectronics and Robert Bosch are respectively the third and fourth largest MEMS players in terms of sales.

Will Europe become the triple threat (ICs, MEMS, and PV)? Only time will tell as European companies continue to diversify and grow in these markets. Faced with tough competition from other regions, Europe does have a strong R&D infrastructure and, therefore, potential for additional revenue and market share.

Portions of this article were derived from the Fab Capacity Report, Equipment Market Data Subscription, and the Global MEMS/Microsystems Markets and Opportunities. These reports are essential business tools for any company keeping track of the semiconductor equipment and material market in Europe. Additional information regarding this report and other market research reports can be found at www.semi.org/marketinfo. If you would like a brochure or a sample of any of these reports, please feel free to contact Edwin Hall ([email protected]).

* Note: that this includes all equipment, used and new. The SEMI consensus reports new equipment and forecast predicts 5 % growth in 2008