MILPITAS, Calif. – April 10, 2024 – Worldwide sales of semiconductor manufacturing equipment edged down 1.3% to $106.3 billion in 2023 from an all-time record of $107.6 billion in 2022, SEMI, the industry association representing the global electronics design and manufacturing supply chain, reported today. The data is now available in the Worldwide Semiconductor Equipment Market Statistics (WWSEMS) report.

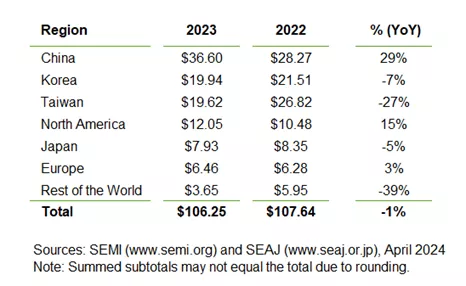

China, Korea and Taiwan – the top three regions in chip equipment spending in 2023 – accounted for 72% of the global equipment market, with China remaining the largest semiconductor equipment market. The pace of investments in China accelerated 29% year-over-year, reaching $36.6 billion in billings last year. Equipment spending in Korea, the second-largest equipment market, fell 7% to $19.9 billion on softer demand and the memory market inventory correction. After posting four straight years of growth, equipment sales to Taiwan also contracted 27% to $19.6 billion.

China, Korea and Taiwan – the top three regions in chip equipment spending in 2023 – accounted for 72% of the global equipment market, with China remaining the largest semiconductor equipment market. The pace of investments in China accelerated 29% year-over-year, reaching $36.6 billion in billings last year. Equipment spending in Korea, the second-largest equipment market, fell 7% to $19.9 billion on softer demand and the memory market inventory correction. After posting four straight years of growth, equipment sales to Taiwan also contracted 27% to $19.6 billion.

Annual semiconductor equipment investments in North America rose 15%, largely on the strength of CHIPS and Science Act investments, while Europe logged a 3% increase. Sales to Japan and the Rest of World decreased 5% and 39% year-over-year, respectively.

“Despite a slight dip in global equipment sales, the semiconductor industry continues to show strength, with strategic investments fueling growths in key regions,” said Ajit Manocha, SEMI President and CEO. “The overall results for the year were better than anticipated by most industry followers.”

Global sales of wafer processing equipment rose 1% in 2023, while other front-end segment billings grew 10%. After contracting in 2022, assembly and packaging equipment sales extended their decline, decreasing 30% in 2023, while total test equipment billings contracted 17% year-over-year.

Compiled from data submitted by members of SEMI and the Semiconductor Equipment Association of Japan (SEAJ), the WWSEMS report is a summary of the monthly billings figures for the global semiconductor equipment industry.

Annual Billings by Region in Billions of U.S. Dollars with Year-Over-Year Change Rates

The SEMI Equipment Market Data Subscription (EMDS) provides comprehensive market data for the global semiconductor equipment market. The subscription includes three reports:

- Monthly SEMI Billings Report, a perspective on equipment market trends

- Monthly Worldwide Semiconductor Equipment Market Statistics (WWSEMS), a detailed report of semiconductor equipment billings for seven regions and 24 market segments

- SEMI Semiconductor Equipment Forecast, an outlook for the semiconductor equipment market

Download a sample of the EMDS report.

For more information about the report or to subscribe, please contact the SEMI Market Intelligence Team at [email protected]. More details are also available on the SEMI Market Data webpage.

About SEMI

SEMI® is the global industry association connecting over 3,000 member companies and 1.5 million professionals worldwide across the semiconductor and electronics design and manufacturing supply chain. We accelerate member collaboration on solutions to top industry challenges through Advocacy, Workforce Development, Sustainability, Supply Chain Management and other programs. Our SEMICON® expositions and events, technology communities, standards and market intelligence help advance our members’ business growth and innovations in design, devices, equipment, materials, services and software, enabling smarter, faster, more secure electronics. Visit www.semi.org, contact a regional office, and connect with SEMI on LinkedIn and X to learn more.

Association Contact

Michael Hall/SEMI

Phone: 1.408.943.7988

Email: [email protected]