Plunging stock prices and Coronavirus-driven business shutdowns presently dominate the news. Current economic data, including the recently released February Global Purchasing Manager Index, support earlier negative predictions of an imminent industry decline.

The recently released February PMI Index dropped sharply, indicating a significant manufacturing slowdown (Chart 1).

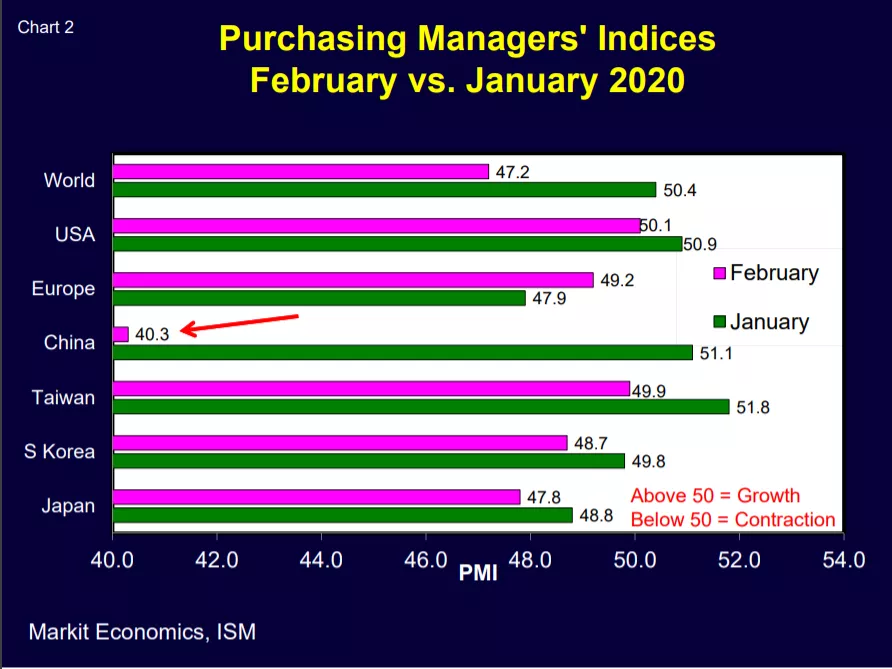

February PMI values varied significantly by country (Chart 2) but China stood out, dropping from PMI=51.1 (slight expansion) in January to PMI=40.3 (sharp contraction) in February – results that support the widely reported abrupt slowdown in overall mainland China manufacturing activity.

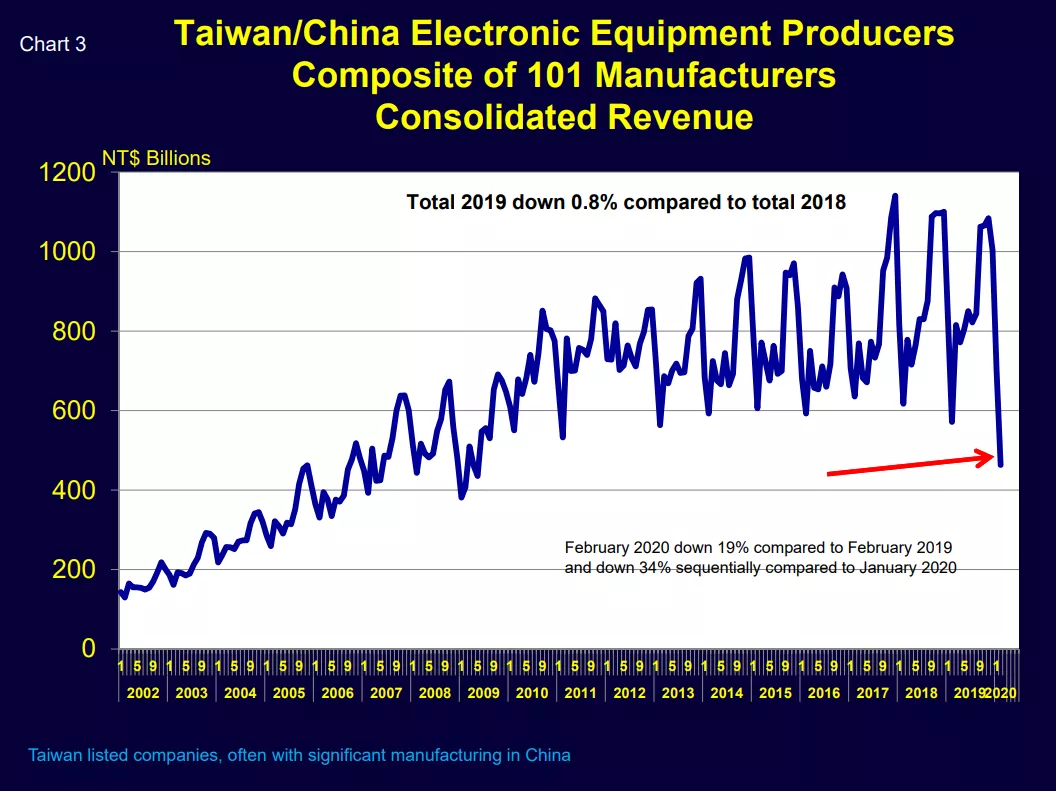

China’s electronic sector output was hit hard in early 2020. Composite sales of 101 Taiwan stock exchange listed OEMs (many of which manufacture on the China mainland) dropped 19% in February 2020 vs. February 2019, a much larger decline than the normal winter seasonal downturn (Chart 3). Recent reports say that some factories are now restoring operations, but the first quarter was certainly very difficult.

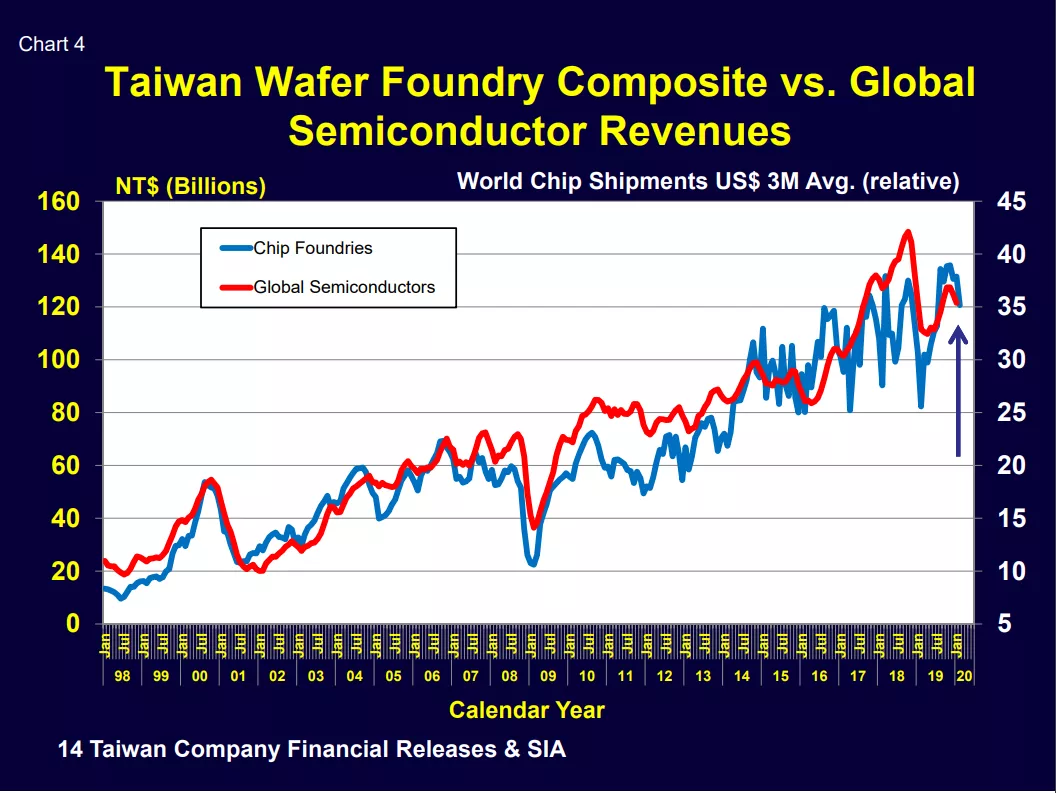

China/Taiwan chip foundry sales (a leading indicator of global semiconductor shipments) also saw a February sales decline following what appeared to be a recovery in late 2019 (Chart 4).

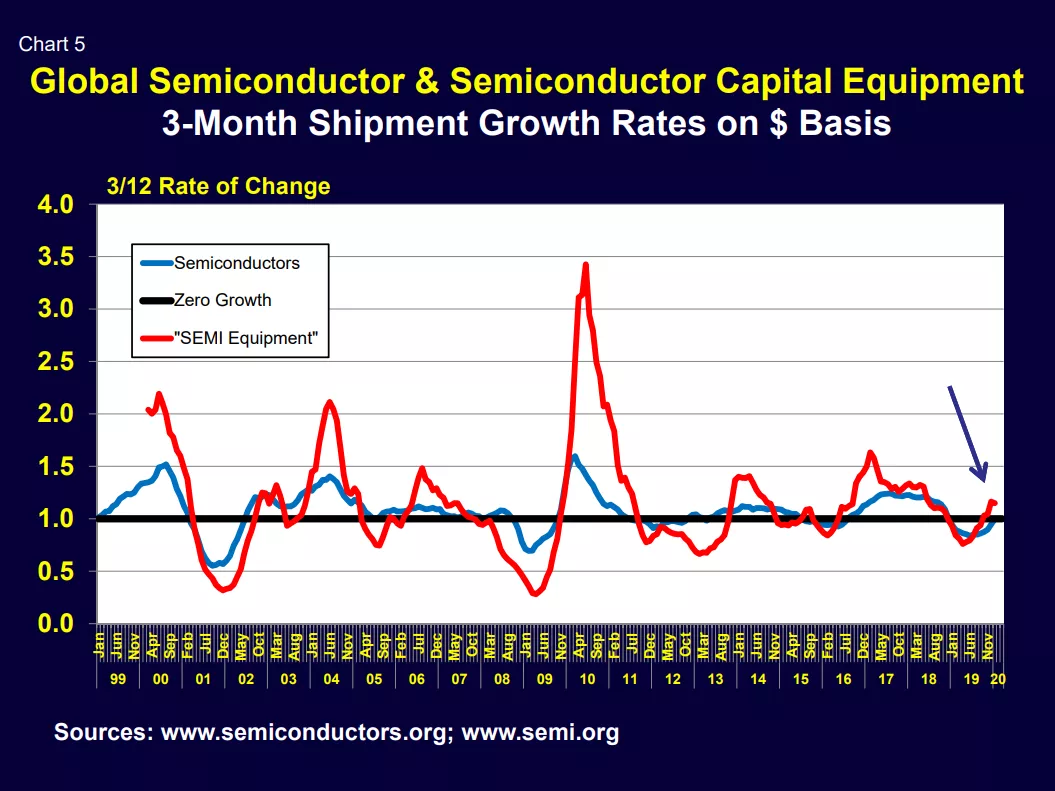

Based on January data (Chart 5), world semiconductor shipments and SEMI capital equipment sales growth had appeared to have recovered, but it is now likely that the February and March semiconductor and semiconductor capital equipment results will be more sobering.

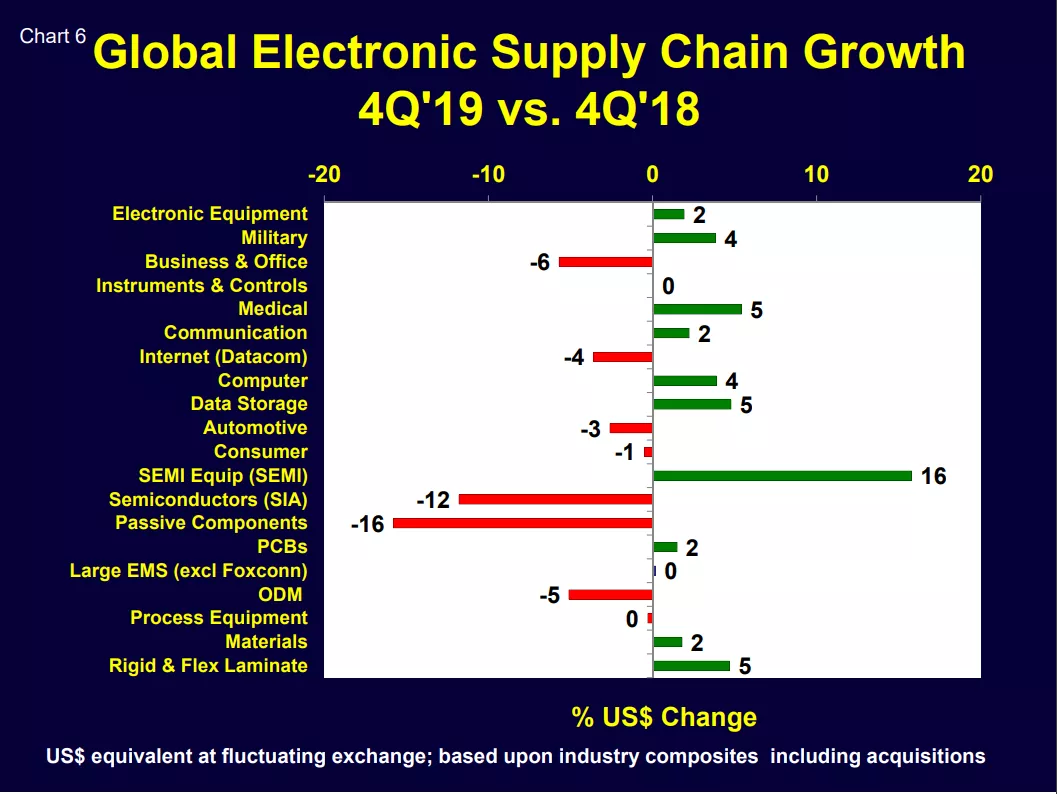

Chart 6 shows the 4Q’19 vs 4Q’18 growth of the global electronic supply chain. We expect the first and second quarter growth rates of 2020 will be much more subdued.

Walt Custer of Custer Consulting Group is an analyst focused on the global electronics industry.

The latest SEMI event scheduling updates are available at Coronavirus Status Updates.