Recent Forecasts

The World Bank just updated its global GDP forecast. Use the link on Chart 1 to download its report “Global Economic Prospects – Heightened Tensions, Subdued Investment."

In this report the World Bank noted that global growth in 2019 has been downgraded to 2.6%, 0.3 percentage point below previous forecasts, reflecting weaker-than expected international trade and investment at the start of the year. Growth is projected to gradually rise to 2.8% by 2021, predicated on continued benign global financing conditions, as well as a modest recovery in emerging market and developing economies (EMDEs).

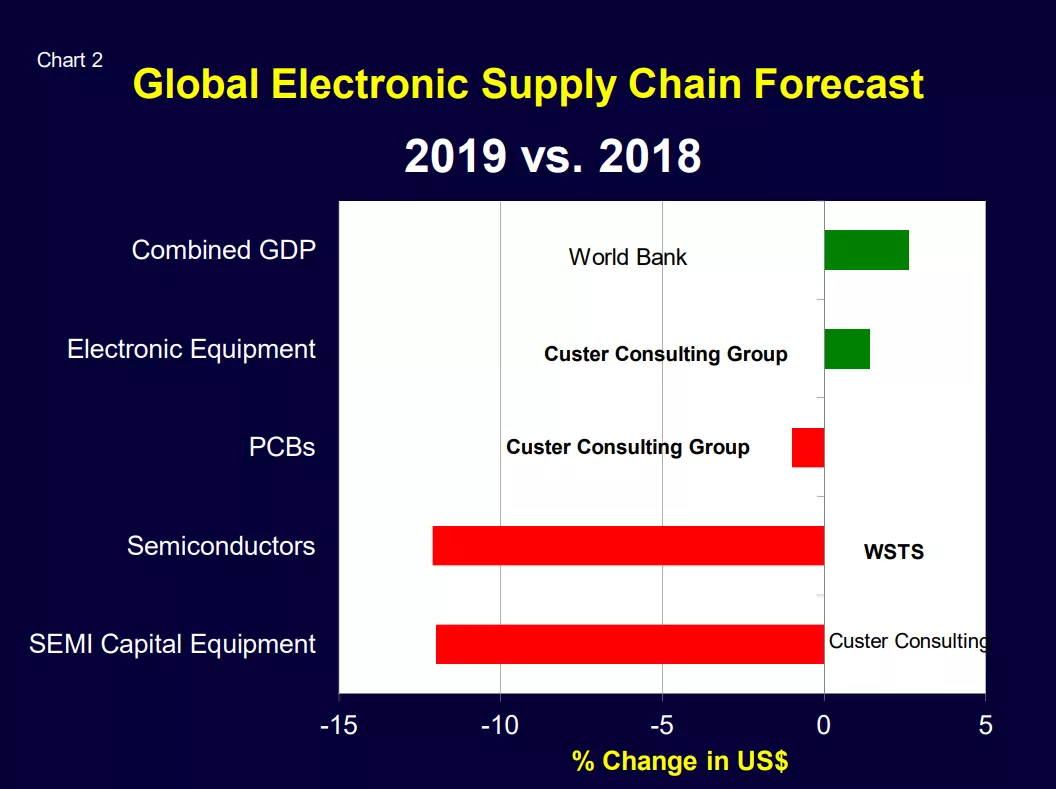

Chart 2 summarizes recent forecasts for key sectors of the global electronic supply chain. Semiconductors and semiconductor capital equipment shipments are both projected to decline 12% in 2019 vs. 2018.

End Market Growth

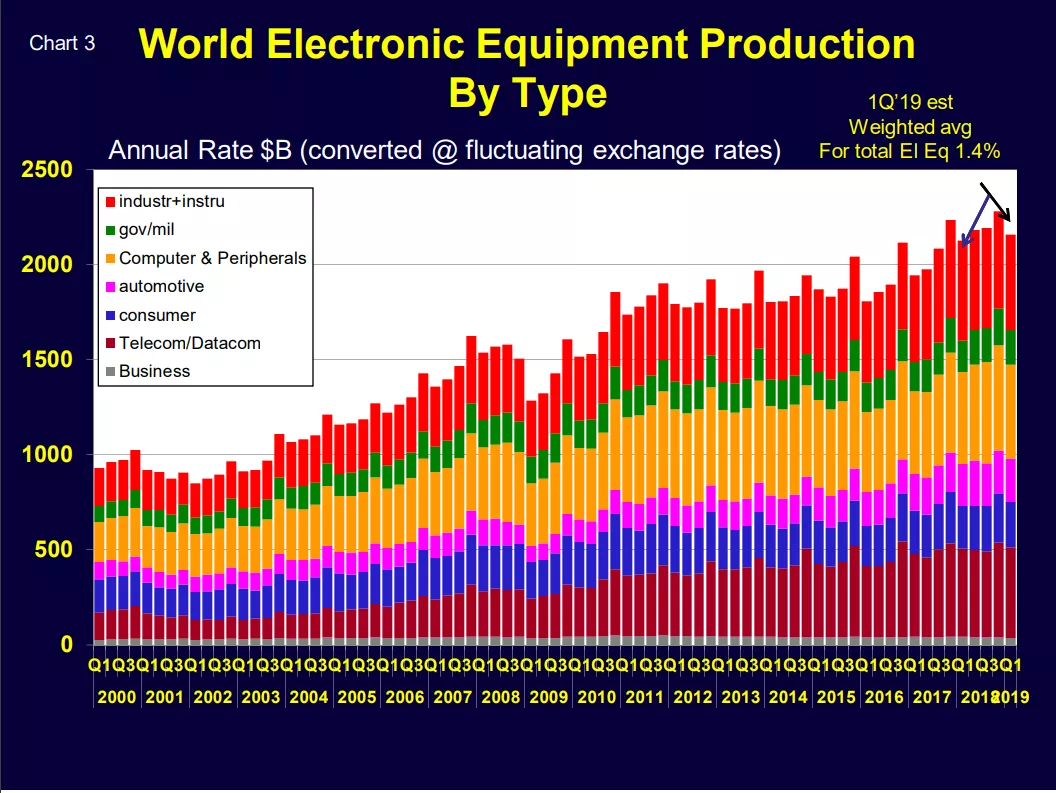

Electronic equipment growth continues but at a more modest pace. Based on the first quarter financial reports of 213 global electronic equipment suppliers, their combined revenues rose 1.4% in 1Q’19 vs. 1Q’18 (Chart 3).

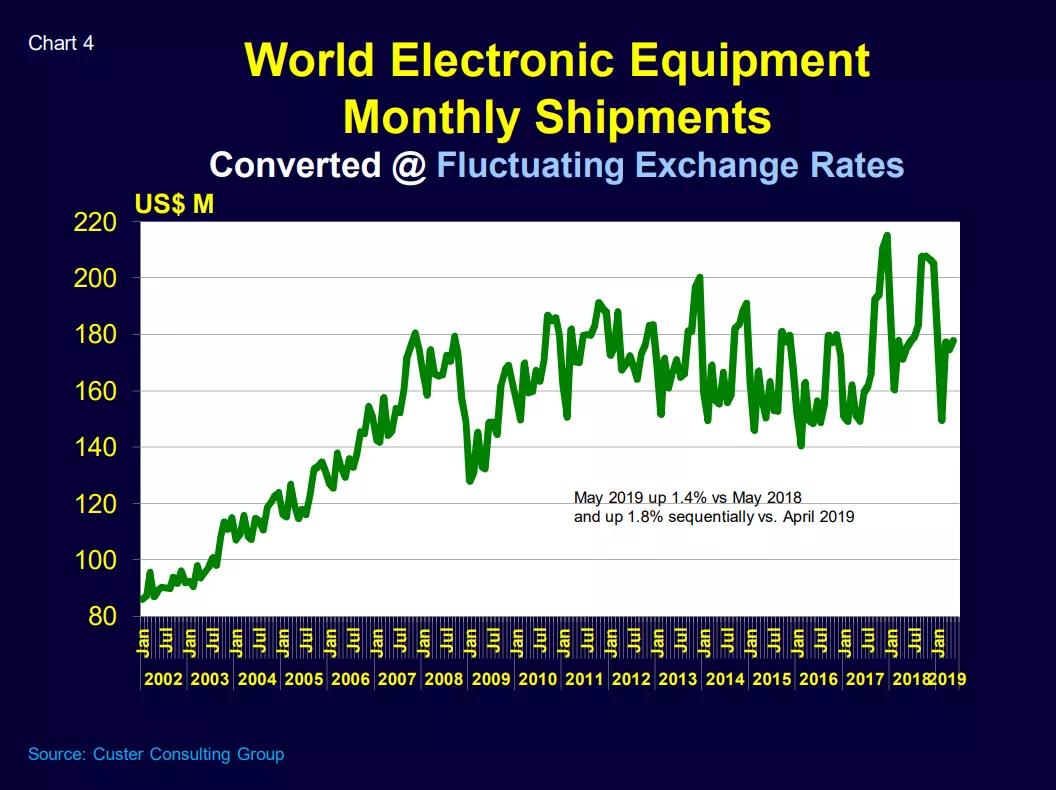

Based on consolidated regional data, combined electronic equipment sales rose 1.4% in May 2019 vs. May 2018 and also increased 1.8% sequentially from April to May 2019 (Chart 4).

Semiconductor Industry Outlook

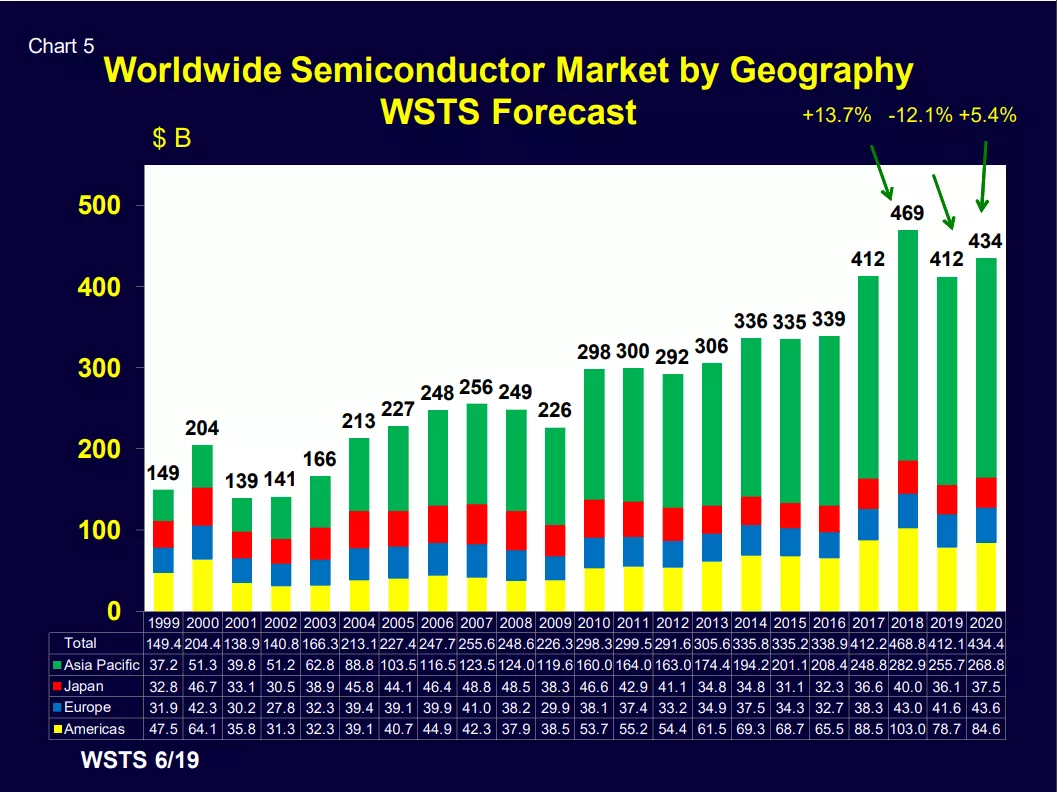

Both the WSTS & SIA in early June endorsed a June forecast projecting that global semiconductor shipments would decline from $469 billion in 2018 to $412 billion to 2019 (Chart 5).

Also in June, SEMI predicted that global fab equipment spending would decline 19% to US$48.4 billion in 2019 before rebounding in 2020, rising 20% to US$58.4 billion.

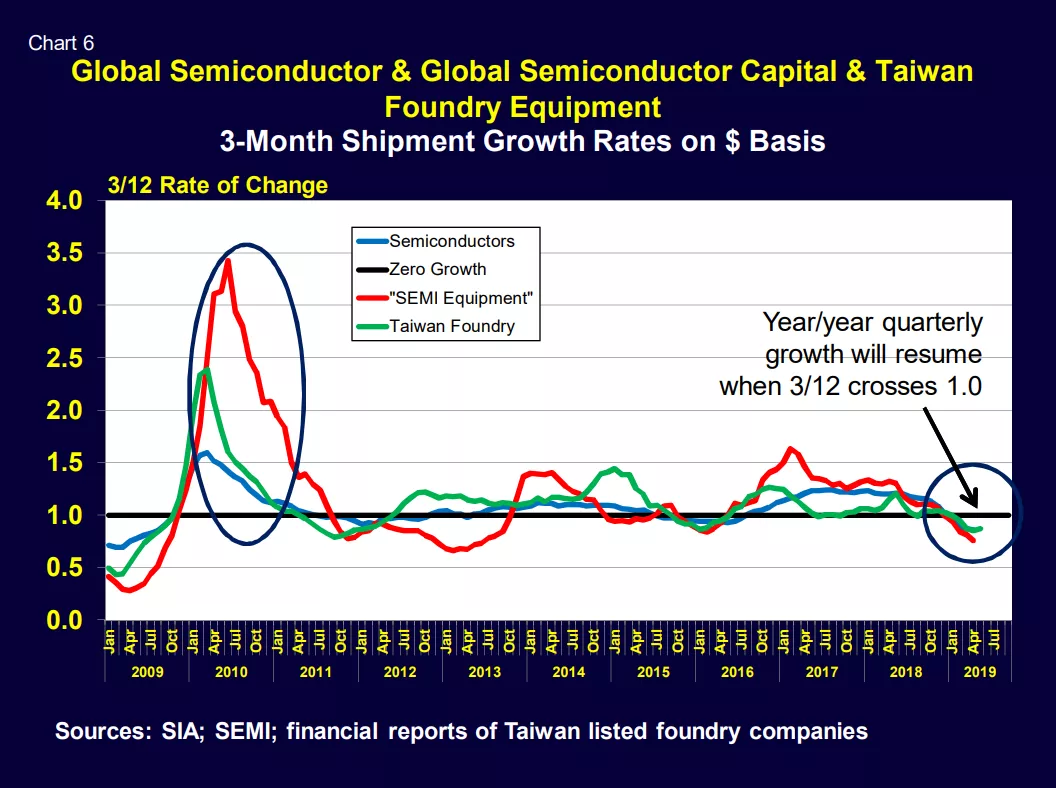

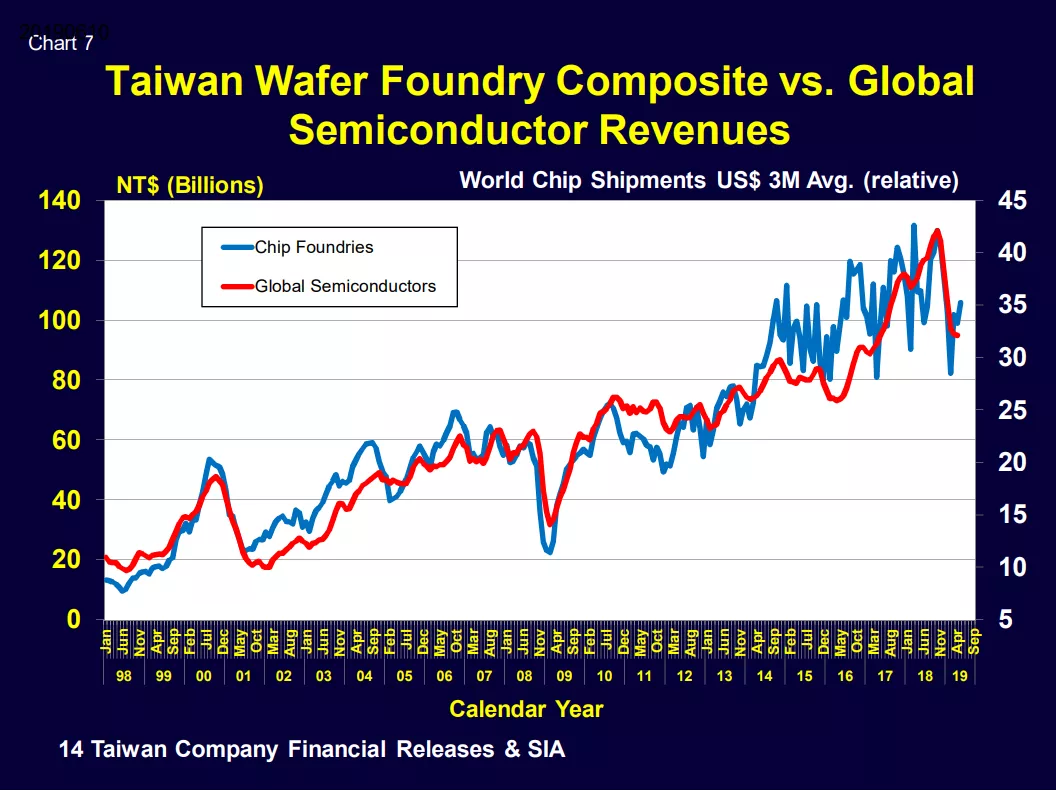

Tide is Turning

Taiwan wafer foundry shipments are a leading indicator of global semiconductor and SEMI equipment revenues (Chart 6). These foundry sales rose in May (Chart 7).

There is a glimmer of light at the end of the tunnel. But most electronic industry time series will likely struggle at least though autumn.

Walt Custer of Custer Consulting Group is an analyst focused on the global electronics industry.